Reasons why Venky’s Stock is going up so fast.

Small Cap: (Rs. 3,960 Cr only)

Industry: FMCG (Chicken and Eggs)

Rated: Good Stock Quality

Fair Valuations at CMP of Rs. 2810.90 with PE of 24.37 compared to industrial PE of 55.86.

POSITIVE FINANCIAL TREND

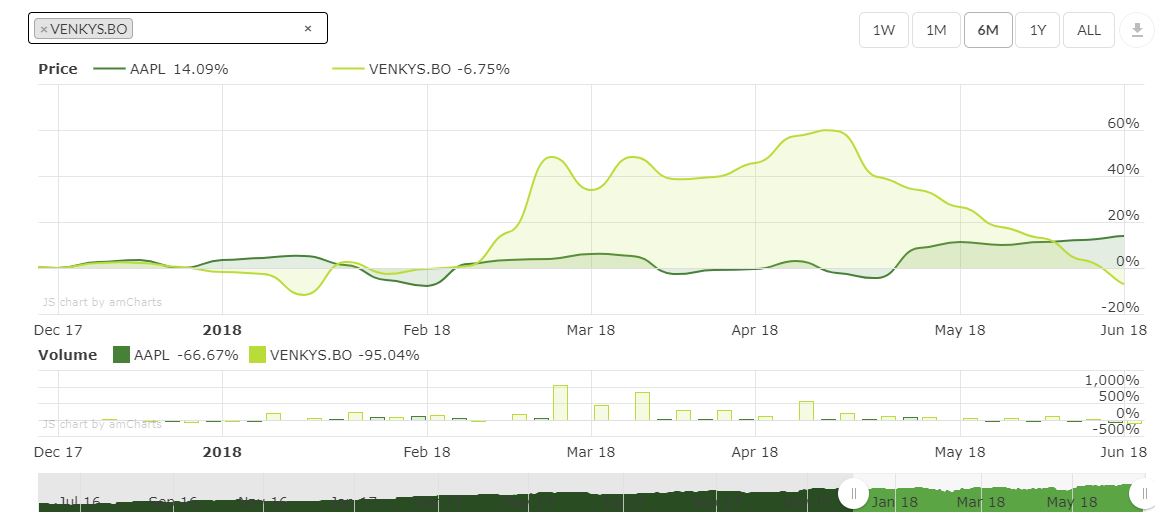

It’s price has increased by a whopping 509.87% while its earnings has increased by 176.42%. Still, it will become expensive in valuations only above Rs. 20,354 as per current EPS and hence has a huge price improvement band left from it’s current market price (CMP) of Rs. 2,810.90.Winter is close by and historically it leads to higher consumption of eggs and chicken leading to higher pricing and hence higher profitability for the company.

|

There’s more stress on Chicken Meat instead of mutton, pork and other meat forms, especially due to the closure of any slaughter houses which led to much higher chicken volume. As a rule of thumb, urban population tends to go for more chicken/egg (Easy to digest ) than rural population, which still prefer mutton. Higher GDP means more urbanization and hence probably more shift to chicken consumption.

With GST and urbanization, organised players will always grow much more than unorganized players benefiting Venkys much more than the industry average. Operating Cash Flow is highest at Rs. 211.36 Cr and has grown in each of last three years. Also, it has increased by a whopping 290% from the last year(2016) Operating Cash Flow of Rs. 78.17 Cr. Half Yearly Debt to Equity Ratio is the lowest in the past five half years at just 0.48 and also has been consistently reducing in each of the past five half years. Half Yearly RoCE (Return on Capital Employed) was highest in last five half years at a whopping 38.17% and has been consistently increasing on each of these past five half years.

Dividend Per Share is highest in last five years at Rs. 6 Per Share.

Half Yearly Cash and Cash Equivalents is lowest in past six half years at just Rs. 155.53 Cr due to higher Capex Spending.

Quarterly PAT has fallen by 20% over the average PAT of the previous four Quarters at Rs. 27.4 Cr and most importantly, Near Term PAT trend is “Very Negative”.

Recommendation: Buy at CMP as well as at Dips. Just keep an Eye on Quarterly PAT and invest for long term. May become a multibagger if held for 3-5 Years.

CMP: Rs. 2,810.90.

Recommendation date: 03/12/2017

Recommended by: Financial IQ Wealth Management Services

| Financial Information |

Corporate Governance

|

| Investor Communication |

| Share Information |